�����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

contents

ENERGY EFFICIENCY

Industry

Energy Service Company (ESCO)

ENERGY EFFICIENCY

Industry

Energy Service Company (ESCO)

Energy Service Companies (ESCO)

Purpose

KEA provides loans to projects where Energy Service Companies (ESCO) replace inefficient facilities of energy consumers who lack technology and financing and guarantee reduction in their energy consumption. KEA also operates and manage registered ESCO

History

-

- ESCO mechanism was originated in the US in late 1970’s as a new investment method for energy conservation projects.

-

- The mechanism was adopted to create economy and society that consume less energy.

- The amendment to the Energy Use Rationalization Act in 1991 provided legal basis for the ESCO program.

- Four companies first registered as ESCO in 1992.

-

- ESCO program was developed to bring in more voluntary participation of private entities, shifting the initiative from the government to the private sector.

Details

Definition

-

What is ESCO (Energy Service Companies)?

-

- ESCO is a company equipped with required facilities, capital and technology and registered to the Ministry of Trade, Industry and Energy pursuant to the article 25 of the Energy Use Rationalization Act and the article 30 of the Enforcement Decree of the same Act.

-

Scope

-

- Cost of the facility (secondhand facilities are not applicable) and supplementary equipment, cost of construction and installation, cost of design and supervision (royalty for technology included), and start-up costs

-

Terms

-

- Interest rate : Quarterly adjustable rate linked to average rate of return of 3 year negotiable Korean treasury bond or fixed-rate

-

- Terms of repayment : Payable in installments in five years with a three-year grace period

-

- Limit : Maximum 30 billion won (Maximum 15 billion won for the same business premise)

Eligibility

-

Scope of the eligible projects

-

- Management services for energy conservation

-

- Investments in energy-saving facilities

-

- R&D of energy-saving facilities and equipment

Details

-

Roles of ESCO

-

- ESCO conducts site surveys for replacement or upgrade of existing energy consuming facilities, make business proposals, provide draft and detailed designs, construct and install facilities, perform a test run and provide maintenance and follow-up management service.

-

Business areas ESCO

-

- Projects to replace existing facilities with energy-saving facilities

-

- Investments in demand-side management projects such as installing air-conditioning systems that run on non-electricity energy sources

-

- Production industrial process improvement projects and waste heat recovery facility installation projects

Concept of the ESCO investment projects

-

Energy users want to replace obsolete and low-efficiency facilities with high efficiency facilities for energy conservation. But they may not have technological or financial capacity to execute such projects.

-

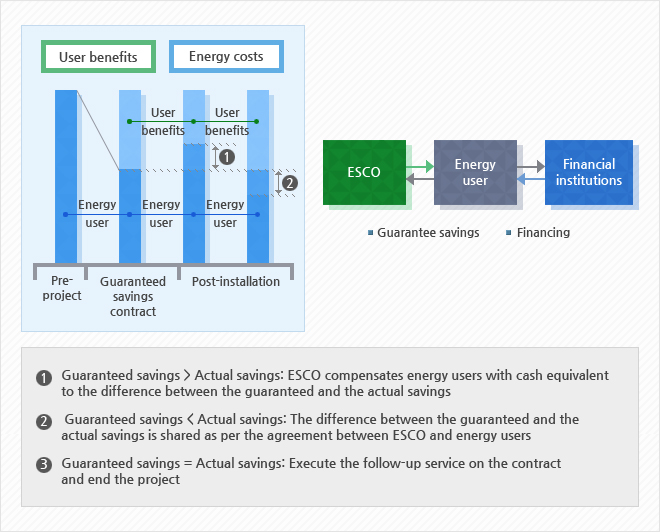

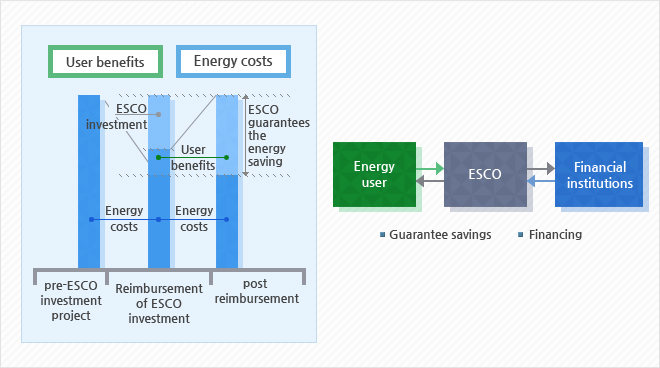

- ESCOs obtain financing for the installation of energy saving facilities (financing is obtained by energy users in case of guaranteed savings contract), execute the project, guarantee energy savings and share the energy cost savings with energy users.

-

- Energy users redeem the investment cost with their energy cost savings

-

- Energy users can replace their old facilities with energy-saving facilities without having to bear financial and technological burden

-

Pros of the investments in facilities through ESCO projects

-

- Install energy saving facilities and reduce energy costs

-

- Reduce technological risks for the investment in the energy saving facilities

-

- Receive systematic and expert service on energy-saving facilities provided by ESCO

-

- Receive financial supports and Tax incentives in connection with ESCO projects

ESCO Contract Scheme

Conceptual diagram of Guaranteed Savings Contract

Conceptual diagram of New Shared Savings Contract

Registration criteria of ESCO and Currently Registered Companies

-

ESCO registration criteria

ESCO registration criteria

| Category |

Details |

Criteria |

| Equipment |

1. Infrared thermometer |

More than 1 thermometer |

| 2. Data recorder |

More than 1 recorder |

| 3. Temperature humidity meter |

More than 1 meter |

| Assets |

Corporation |

Capital |

Over 200 million won |

| Individual |

Appraised value of assets |

Over 400 million won |

| Technical talent |

Construction engineering, mechanical engineering,

material engineering, chemical engineering,

electrical/electronic engineering and energy or gas

prescribed in the National Technical Qualifications Act |

More than 3 engineers |

Tax incentives (income tax or corporate tax deduction)

-

Legal basis for the Tax incentives for the companies invested in energy saving facilities thorough ESCO was established in January 1998

-

Legal basis for the Tax incentives for the SMEs invested in energy saving facilities through ESCO was established in 2010

-

Tax deduction for SMEs

-

- Pursuant to the article 5 of the Special Tax Treatment Control Act, the amount equivalent to the income of SMEs multiplied by income tax or corporation tax deduction rate is deducted for the relevant taxation year by December 31, 2015.